Peak Gold or Andean Results Confirm Gold Corp Over-paying.

By: Marco G.

October 8th, 2010

http://goombarhsedge.blogspot.com/

Introduction

Andean Resources (ANDPF.PK, TSX:AND) issued a news release yesterday with results from their 72 drill holes since their previous July 19th release . The results were interesting gold drilling wise but mundane in terms of adding spectacular value for Andean and only served to confirm what the author already expressed about Gold Corp (GG, TSX:G) over paying for this acquisition in this editorial here.

In my previous criticism, the author asserted that Gold Corp was paying $1619 per reserve ounce for Andean’s kitty of 2.1 million ounces and that was way too much.

The author is not a geologist, and speculates that even if the new drill results will change all the previous NI 43-101 3.1 million compliant resources into minable reserves, the resulting price of $1096 per reserve Gold ounce is still too much.

The high price per reserve ounce that Gold Corp is willing to pay is indicative of the large gold companies operating environment presently and serves to underscore their desperate battle to maintain their market value in the face of mined out reserves and increasing mining costs.

Peak Gold or Mined Out Reserves

Aaron Regent, president of Barrick Gold (ABX, TSX:ABX) the world’s largest gold producer made a surprising announcement last fall regarding their Gold mining business. He told an English audience in 2009 at a Gold Conference in London that:

“There is a strong case to be made that we are already at peak gold,” Regent said. “Production peaked around 2000 and it has been in decline ever since. And we forecast that decline to continue as it is increasingly difficult to find ore.”

Global Gold output has been in decline since 2000-2001. The declines average 5% per year and is a factor in the Gold’s price quintupling since then. For example the production output from North America has decline by an astonishing 60% over the last decade.

The days of easy Gold discovery and cheap Gold production days are gone.

Peak Oil or Rising Production Costs

Mining with the moving and excavation of mountains of materials, is in itself is an extraordinarily energy intensive business. Note the energy problems that surfaced in South Africa, last year, as Eskom their power utility, cut back their services and increased their service rates. This caused the whole family of South African miners to suffer severe problems and reduced their market capitalization across the board.

Noted economist Dian Chu recently penned in her Seeking Alpha article a prediction of $100 per barrel of Oil:

But the longer term trend is clear as traders and fund managers want to be strategically exposed to Oil from this point forward, as the real upward move is just now starting, expect crude oil to hit $100 a barrel by January, and only going higher from there.

Oil prices factor directly into mining costs and indirectly into the infrastructure and material movement costs of these large mining projects.

The only saving factor for the large Gold miners is that the market price of the Gold precious metal appears to be going up for the longer term.

Market Reception of Large Cap Golds

How has the market been valuing the share prices of these large Gold miners? The author ran a performance chart for the gold ETF GLD, the large miners index HUI, the quality Gold miner Gold Corp, and the junior Gold miners ETF GDXJ as follows: (click to enlarge)

In this year-to-date price performance comparison, the GLD ETF, the red trace has gained about 22%. The surprising fact is that the blue trace, the HUI large gold miners index has only gained about the same 22% as the Gold price. Then we see that the green trace, Gold Corp was fairly equal with both GLD and HUI until September, when it drops off to show a total year-to-date gain of about 15%. The Gold miners Junior ETF the GDXJ has gained a chart leading 40% for the year.

Is this surprising to the reader? Even with the higher Gold prices, and increased profits, the large miners, such as Newmont (NEM) are reporting increased operating costs, and their share prices are stagnating.

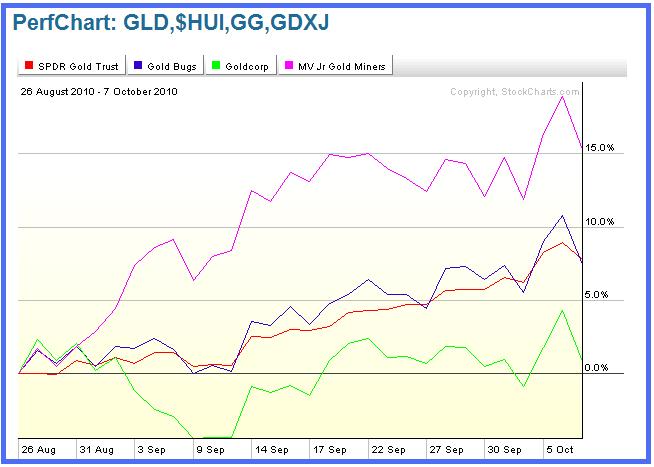

For a closer look at these miners during the recent Summer’s end run-up in the price of Gold, the author ran a second performance chart for the last six weeks as displayed following: (click to enlarge)

During this shorter time period the performers were in the same sequence as in the previous chart. During the last six weeks, Gold has increased in price about 7.5% together along with the HUI index’s increase of 7.5%. Note that the blue HUI line is more volatile relative to the red GLD line. The HUI both undershoots and overshoots the red GLD price line.

Gold Corp’s price went nowhere and stayed the same. The market is showing uncertainty about the value of Gold Corp purchasing Andean Resources.

Finally though, look at the performance of the GDXJ ETF. This collection of 60 junior Gold companies with market capitalizations of mostly under $1 Billion dollars shows a spectacular leverage to the price of Gold. The GLDJ shows a 15+% increase relative to Gold’s GLD about 7% increase for a leverage of about 100% more gains.

This second look serves to confirm the first chart’s observations.

Conclusions

Peak Gold together with Peak Oil is upon us and may force investors to look at the precious metals markets differently. The irrational or possibly rational market is not valuing major Gold producers as good investments presently. The price charts evidence shows that investors might just as well just place their monies in the Gold metal itself, as the major caps are certainly providing no leverage at all to the metal price. Investing in the gold equities would also bring on extra companies’ risk such as exhibited by Gold Corp with their acquisition of Andean and the resulting price decline.

The second piece of price performance evidence is that the junior Gold producers are hot. They as a group are providing investors with a doubled leverage to the underlying Gold price. This should be noted by astute investors, as this junior Gold producer segment is where the market valuation changes are happening right now.

No comments:

Post a Comment